I’ve seen plenty of cycles since I started out in mortgage brokering. Rates going up, rates coming down, rules changing. But I have to admit it: I had never seen the market shift as fast as it has over the past few months. And while everything is moving, most people keep making mortgage decisions as if nothing had changed.

In this article, I walk you through five truths your bank won’t tell you in 2026: why your file is being scrutinized like never before, why the famous 20% down payment threshold isn’t always the right target, why variable rates are making a strong comeback, why the first renewal offer is never the best one, and why your house, on its own, won’t fund your retirement. Along the way, I’ll also share two ideas the industry is debating: the return of the 35-year amortization, and the case for a separate benchmark rate for housing. No pointless jargon, I promise. Just what I tell my clients, numbers in hand, when they sit down across from me.

Why is your bank going over your file with a magnifying glass in 2026?

Let’s start with a number that makes your head spin. The uninsured mortgage market now exceeds $1,000 billion in Canada. Yes, one trillion dollars. It’s now the majority of residential lending in the country.

A quick refresher so we’re on the same page. When your down payment is under 20% of the purchase price, your loan has to be insured — by CMHC, Sagen or Canada Guaranty. That insurance protects the lender if you stop paying. On an uninsured loan, by contrast, the bank absorbs the entire loss on its own if you default.

For a long time, a good share of Canadian homeowners carried an insured mortgage. That era is behind us. And a lender carrying all the risk inevitably becomes pickier. In practice, that means tighter income verification, more conservative property appraisals, and far less flexibility for anyone whose profile doesn’t fit the mold: self-employed workers, newcomers, commission or rental income.

I see it every week in the files that cross my desk. A file that would have sailed through three years ago now gets sent back over a missing bank statement. The good news? When one institution says no, another may very well say yes. You just have to know which door to knock on. That’s exactly what a mortgage brokerage service is for.

Do you really need a 20% down payment?

Here’s the mistake I see most often, by far. Buyers who drain every account, push their project back a year or two, sometimes even liquidate their investments — all to hit the famous 20% mark and avoid the insurance premium. On paper, it sounds perfectly sensible. Once you run the numbers, it’s a different story.

Let’s first look at what the insurance actually costs. With a 10% down payment, the CMHC premium is 3.10% of the amount borrowed on a 25-year amortization, and 3.30% if you go with 30 years, since CMHC adds 0.20 points for extended amortizations. On a $500,000 purchase with $50,000 down, that comes to roughly $13,950 over 25 years and $14,850 over 30 years, usually added to the loan and amortized over its full term.

And that’s not all. In Quebec, this premium is subject to the 9% tax on insurance premiums — about $1,256 on 25 years or $1,337 on 30 years. And unlike the premium, that tax can’t be rolled into the loan: it’s paid in cash at the notary’s office, on closing day. Think about that for a second. We’re taxing an insurance premium that’s supposed to help first-time buyers get into the market? Really? Where’s the logic in that?

That said, let’s keep things in perspective. It’s a real cost — I’m not denying it. But it’s a one-time cost. And here’s a detail few people know: insured loans often get better rates than uninsured ones, precisely because the lender’s risk is covered. Part of the premium effectively pays for itself.

Now let’s look at what the alternative earns you. Take a Quebec household whose income puts it at a marginal tax rate of about 36.5%, which reflects the reality of much of the province’s middle class. Every $10,000 contributed to an RRSP returns roughly $3,650 in tax refunds. That’s an immediate, guaranteed return, before the investment has generated its first dollar of growth.

And growth is worth talking about. Over the past twenty years, the S&P 500 has delivered an annualized return of about 10% with dividends reinvested — around 8.5% after inflation. But what strikes me most in the historical data is something else: in nearly a century, no 20-year period has ever produced a negative annualized return on that index. The worst came in at about 3% per year. The best, at nearly 18%. Nobody knows the future, but a twenty-year horizon smooths out a great deal of the risk.

Let’s run the numbers together on our $500,000 purchase. Option A: you put down $100,000 — 20% — and avoid the premium. Option B: you put down $50,000 — 10% — pay the premium of about $13,950, and the remaining $50,000 goes into your RRSP. At a 36.5% marginal rate, that contribution eventually returns about $18,250 in tax. Enough to absorb the premium, the 9% tax that comes with it, and still keep a surplus.

Want to test these numbers against your own situation?

Purchase price, down payment, marginal tax rate, expected return: our Down Payment Paradox calculator runs the full math in seconds, CMHC premium and 9% tax included.

One important nuance here, because a rushed calculation could cost you dearly: deducting $50,000 all at once is rarely the right move. Why? Because a large deduction pushes your taxable income down into the lower brackets, where each deducted dollar only recovers 31% or 27% instead of 36.5%. The smart mechanics are to contribute now, so the money grows tax-sheltered from day one, but to spread the deduction over two or three years — and split it between spouses where possible. Each of you deducts, each year, only the portion that offsets income taxed at 36% or more. A couple sharing $50,000 and deducting this way captures the full $18,250, sometimes more if one of them sits in a higher bracket. All of this, of course, subject to having the contribution room.

And what if your RRSP room is limited, or your income puts you below the 36% line? The TFSA becomes a very serious alternative, provided you have the room there too. No tax refund going in, true. But growth and withdrawals are entirely tax-free, forever. Invested at the market’s historical pace, $50,000 can more than triple in twenty years, and every dollar of gain is yours in full, with no tax bill on the way out. In short, the RRSP generally wins when your current tax rate is higher than the one you’ll face in retirement, and the TFSA wins on flexibility and simplicity. Either way, the capital is working while the extra interest cost on the portion you didn’t put down runs at a mortgage rate of barely more than 4%.

Homeowners who want to push the optimization even further can also gradually convert their non-deductible mortgage interest into deductible interest while building an investment portfolio. That’s the principle behind the Smith Manoeuvre and the MAPA (its cash-damming cousin), two strategies I practise as an accredited broker. I cover them in detail in our complete guide to the Smith Manoeuvre and the MAPA and in our MAPA vs. Smith comparison, and you can model the strategy with our Smith Manoeuvre calculator.

This strategy isn’t for everyone. It requires genuine risk tolerance, discipline and reasonable job security. It also has to be weighed against the tools reserved for first-time buyers: the FHSA, which lets you accumulate a lifetime $40,000 that’s deductible going in and tax-free coming out, and the Home Buyers’ Plan, whose withdrawal ceiling has risen to $60,000 per person. A couple can now mobilize up to $200,000 in tax-optimized down payment by combining these vehicles — not counting the new relief on the welcome tax I discussed in this recent article. The right answer depends on your marginal rate, your horizon and your profile. It’s exactly the kind of analysis we do together, numbers in hand, before choosing the financing structure.

Fixed or variable: why are variable rates making a comeback?

If you had a variable rate in 2021 or 2022, you still remember it. Going from 1.5% to more than 5% in a matter of months leaves a mark. Several of my clients swore back then they’d never touch one again.

And yet, here they come again. Variable rates accounted for roughly 40% of new applications last May — nearly double January’s share. The reason is simple: fixed rates have climbed back above 4.19%, while variables are being negotiated around 3.60%. More than half a point of spread shows up immediately on the monthly payment. For an in-depth comparison of the two, I’ve devoted a full article to the fixed vs. variable question in Canada, and you can check our current rates anytime.

Before jumping on a variable, though, take the time to check three things. First, a variable isn’t a bet on where rates are headed — it’s a structural choice. Prepayment penalties are generally capped at three months’ interest, whereas fixed rates can expose you to interest rate differentials that are sometimes brutal. If you think you might sell, refinance or restructure before maturity, that’s a huge advantage. Second, not all variable products are created equal: some adjust the payment when rates move, others change the split between principal and interest, and the consequences in a rising-rate scenario are worlds apart. And above all, stress-test your own ability to absorb a payment shock before you sign, not after. It’s an exercise we run systematically with our clients.

Mortgage renewal: why should you never sign your bank’s first offer?

This is the trend with the heaviest consequences, and the one that worries me most. Hundreds of thousands of households that borrowed at pandemic-era rock-bottom rates are coming up for renewal at significantly higher rates. For many, the math simply doesn’t balance anymore.

The Bank of Canada itself is sounding the alarm: in the Toronto area, the country’s largest real estate market, roughly 10% of homeowners would not be able to qualify for a refinance in 2027. Think about what that really means. A borrower who can’t qualify elsewhere is a captive client. Their bank knows it. And a bank that knows you can’t leave has no commercial reason to offer you its best rate.

It’s the industry’s worst-kept secret: the first renewal offer that arrives in the mail is rarely the best one. It’s calibrated for clients who sign without shopping around. Put that same file in front of several competing lenders, and the balance of power changes completely. Even if you end up staying with the same lender, you stay on better terms. To put the odds on your side, see how to prepare your mortgage file properly and our dedicated mortgage renewal page.

And if your situation has weakened in the meantime — lower income, accumulated debts, late payments — know that there are transition solutions through alternative or private lending, including with a damaged credit file. They let you get through the rough patch without selling your home under pressure. I structure these regularly, and believe me, it’s always better to act before receiving a 60-day notice than after. Our mortgage refinancing page details the options.

What if we brought back the 35-year amortization?

The topic has come up in almost every conversation I’ve had these past few months. Budgets cracking, loans being stretched, and a question hanging in the air: why cling to the sacred 25 years? Should we reopen the door to 35 years, like before 2011? The question deserves better than a knee-jerk answer. Let’s take the time to unpack it.

Why is this debate back now?

First, let’s set the scene. The Bank of Canada has held its policy rate at 2.25% since June, and 5-year insured fixed rates are hovering around 4%. Affordability is improving a little, that’s true. But the real stress of 2026 is the renewal shock: a large share of households is renewing loans taken out when the policy rate was below 1%. And there’s something deeper still. Home prices have drifted far away from wages over the past fifteen years. When the gap between house prices and incomes widens year after year, should we really be surprised that loan duration becomes the pressure valve?

What would it actually change for a buyer?

Let the numbers talk. On a $400,000 loan at 4%, the monthly payment goes from about $2,110 over 25 years to roughly $1,910 over 30 years, $1,770 over 35 years and $1,670 over 40 years. For a first-time buyer bumping up against the stress test, those few hundred dollars a month make all the difference between qualifying and staying a renter. To see where you stand, read our article on how to calculate your borrowing capacity, or go straight to a pre-qualification before your purchase offer.

And let’s be honest with each other: the 25-year rule is already, in part, a regulatory fiction. In real life, Canadians’ effective amortization often exceeds 25 years. We refinance, we stretch at renewal, and banks even tolerated negative amortizations on variable rates in 2023. Meanwhile, the alternative market already offers 40 years on conventional loans. Making an insured 35-year official — wouldn’t that simply align the rule with reality on the ground?

So where’s the catch?

It’s very real, and it comes down to one word: supply. Canada’s problem is first and foremost a housing shortage. What happens when you increase every buyer’s borrowing capacity at the same time, in a market where supply can’t keep up? The gain gets capitalized into prices, usually within 12 to 24 months. The first-time buyer ends up with the same monthly payment for the same house, but with more debt on their shoulders. That’s exactly what we observed, at least in part, after the December 2024 reform, when the 30-year option was broadened and the insurable ceiling raised to $1.5 million.

And the total cost — do we really grasp its scale? On that same $400,000 loan, we’re talking about roughly $233,000 in interest over 25 years, versus close to $400,000 over 40 years. Almost double. The figure makes people jump, and that’s normal.

But before closing the file, let’s ask a question almost nobody asks: will a dollar today still be worth the same in 10, 20, 30 or 40 years? Of course not. The Bank of Canada targets 2% inflation per year, and at that pace, prices double roughly every 35 years. In other words, a dollar loses about half its purchasing power over that period. Doubtful? Ask your parents what their grocery basket cost in the 1980s. Or think back to the family home bought for $75,000 back then — the one worth several hundred thousand dollars today. The salary paying off your mortgage in 30 years won’t be today’s salary either. Concretely, the $1,670 payment in the final year of a 40-year loan would only weigh the equivalent of about $750 in today’s dollars if inflation stays on target. A good part of those famous $400,000 in interest will therefore be paid in dollars far lighter than the ones coming out of our pockets right now.

Does that erase the gap? No, and it has to be said with the same honesty. Even in constant dollars, the 40-year bill remains clearly higher than the 25-year one. And two realities remain, whatever inflation does: equity builds very slowly during the first ten years of a long amortization, which leaves the owner exposed if prices correct, and the longer the amortization stretches on insured lending, the more the risk shifts onto the taxpayer, through CMHC. Inflation softens the bill. It doesn’t make it disappear.

Would a well-framed 35-year be the right compromise?

Here’s where I land, after turning the question over every which way. A targeted return to 35 years would make sense: first-time buyers and new construction only, on the model of 2024’s 30-year change. Targeted at new builds, the inflationary effect is smaller and you stimulate supply in the process. It’s also worth knowing that the returns diminish quickly: going from 25 to 30 years cuts the payment by about 9%, from 30 to 35 years by about 7%, and from 35 to 40 years by barely 5.5%. A generalized 40-year, on the other hand, would cost dearly in debt for an affordability gain largely absorbed by prices. We’d be replaying the 2006–2008 movie, and we know how it ends.

The real breathing room for young households will come from supply and incomes, not loan duration. But between a dogmatic 25 years and the pre-crisis 40, a well-framed 35-year strikes me as a defensible compromise. And something tells me this debate will be back on the table if the 2026 and 2027 renewals hurt as much as we fear.

One rate for the economy, one rate for mortgages: crazy idea or serious avenue?

Let’s push the thinking one notch further. The Bank of Canada’s policy rate is the lever that steers our entire economy: consumption, investment, the dollar, inflation. One single lever for everyone. But who takes each of its moves the hardest? Mortgaged households.

When a trade war erupts or a political shock derails inflation, the central bank raises its rate to cool the whole economy. And the homeowner who asked for none of it watches their mortgage payment jump by several hundred dollars a month. Their financial stress doesn’t come from their choices, but from global events over which they have no control whatsoever. Is that really the fairest mechanism we can imagine?

So let’s ask the uncomfortable question: could the two be separated? A benchmark rate designed for residential mortgage credit — more stable, smoothed over time — and another rate for the rest of the economy? No major central bank operates that way today, and economists would see enormous implementation challenges, starting with the risk of distortions between credit markets. But let’s remember that other tools once deemed unthinkable eventually came to be: the stress test, mandatory loan insurance, amortization caps. When hundreds of thousands of families see their budget upended by decisions made thousands of kilometres from their kitchen, the question at least deserves to be asked. I’ll leave it open, and I’d sincerely love to read your reactions in the comments.

Will your house be enough to fund your retirement?

Our parents burned their mortgage at 55. That model is disappearing before our eyes: mortgage balances among 55-to-64-year-olds jumped by about 6% in 2025, and nearly one Canadian in two no longer believes the value of their home will be enough to fund their later years.

The myth of “my house is my pension fund” is dying, and we need to draw the lessons. A house is a wonderful asset — but an illiquid one. It pays no income. It costs taxes, maintenance, insurance. Its value only turns into money at the moment of a sale or a loan. Reaching retirement with a paid-off house but no liquid savings means being rich on paper and squeezed at the grocery store.

So the real question isn’t “will my house be worth enough?” but rather “how do I turn that value into income, at the right time and at the lowest tax cost?” Which brings us straight to the last point.

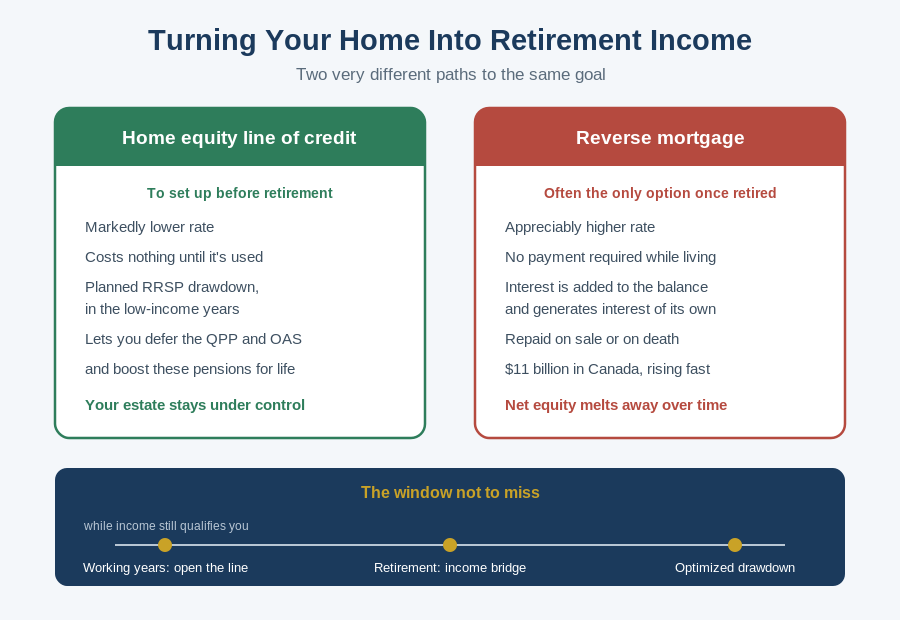

Reverse mortgage or line of credit: which strategy to choose before retirement?

A direct consequence of the above: reverse mortgages are exploding and now represent about $11 billion across the country. The appeal lies in the simplicity. The house pays you. The lender advances you regular sums or a lump amount, no payment is required during your lifetime, and the loan is repaid when the property is sold or upon death.

Easy money today, paid for with tomorrow’s inheritance. That’s how I sum it up for my clients. Reverse mortgage rates are noticeably higher than those of conventional mortgages. And since no payments are made along the way, the interest compounds: it gets added to the balance, which itself generates more interest. Over fifteen or twenty years, the snowball effect can eat away a considerable share of the property’s net value.

Yet there’s a far more elegant strategy, and too few people know it. Remember this: lenders qualify you on your income, not your assets. The day you retire, your borrowing capacity collapses — even if your house is worth a million and your RRSPs are well stocked. It’s the cruel paradox of credit: money is lent to you easily when you don’t need it, and with difficulty when you do.

The solution? Set up a home equity line of credit while you’re still working and your income qualifies you on the best terms. That line costs nothing as long as you don’t use it. But in retirement, it becomes a formidably effective drawdown tool.

First, it lets you choose the timing of your retirement rather than endure it: a cushion of liquidity available at all times is the freedom to leave when you want. Next, it lets you draw down your RRSPs in a planned way: rather than making large taxable withdrawals in the wrong years, you tap the line temporarily and withdraw from the RRSP in low-income years, controlling your tax bracket and avoiding the Old Age Security clawback. Finally, it lets you defer QPP and OAS by a few years — and every year of deferral permanently increases those government pensions.

All of it at a rate well below a reverse mortgage’s, with total flexibility and without eroding the inheritance in an uncontrolled way. But this strategy has an expiry date: it must be put in place before the end of your working life. After that, the door closes.

Key takeaways

- Uninsured mortgages now dominate the market: banks are tightening their file reviews, and atypical profiles have more reason than ever to shop around.

- Chasing a 20% down payment at all costs isn’t always the right call: the RRSP tax refund can absorb the CMHC premium and its tax in the very first year, provided you spread the deduction wisely.

- Variable rates are back in force, around 3.60% versus more than 4.19% for fixed — but it’s as much a structural choice as a rate choice.

- Never sign the first renewal offer: a captive client never gets the best rate, and a file put out to competition changes the balance of power.

- The home equity line of credit is set up before retirement: it enables planned RRSP drawdowns and QPP/OAS deferral, at a far lower cost than a reverse mortgage.

Frequently asked questions

When should I start shopping for my mortgage renewal?

Ideally four to six months before maturity. Most lenders let you lock in a rate 90 to 120 days in advance. If rates rise during that window, you’re protected. If they fall, you benefit from the drop. Waiting for the renewal letter means giving up that safety net.

Does a mortgage broker cost anything?

In the vast majority of residential files, nothing at all. The broker is paid by the lender that funds the mortgage, and the rate you get is the same — often better — than if you negotiated alone. Only certain alternative or private files involve fees, and those are always disclosed up front, in writing.

Can I switch lenders at renewal without starting all over?

Yes, and it’s simpler than it used to be. In most cases, a straight transfer at maturity no longer requires re-passing the stress test, and several lenders cover the transfer fees to attract your file. Every situation has its particularities, which is why it’s worth having yours reviewed before signing anything.

Is it a good idea to put down less than 20% in order to contribute to my RRSP?

It can be — and it’s sometimes clearly more profitable, as the worked example above shows. The tax refund at a 36.5% marginal rate can absorb the insurance premium in the first year, while the capital grows tax-sheltered. But the answer depends on your contribution room, your risk tolerance and your horizon. Have the math done for your specific situation before deciding.

Can you amortize a mortgage over 35 years in Canada?

Not on an insured loan: the limit is 25 years, or 30 years for first-time buyers and new construction since December 2024. On a conventional loan, with 20% down or more, 30 years is common and some alternative lenders offer 35 or even 40 years. These products come with their own conditions and their own costs — all the more reason to have a broker analyze them before committing.

What’s the difference between a home equity line of credit and a reverse mortgage?

The home equity line of credit is set up during your working life, offers a lower rate and leaves you full control of the balance, since you pay the interest as you go. The reverse mortgage can be obtained without income and requires no payment during your lifetime, but its rate is higher and the interest piles onto the balance, eating away at the property’s net value year after year. The first is planned; the second is too often endured.

Will mortgage rates come down in 2026?

Nobody knows for certain, and be wary of anyone who claims otherwise. What we do know is that nothing points to a return to the exceptional conditions of 2021. The best strategy isn’t to guess the direction of rates, but to choose a loan structure that protects you in both scenarios.

The bottom line: make lenders compete

If you take away only one thing from everything above, let it be this: never sign anything without comparing. Not a first renewal offer, not a down payment structure, not a variable product chosen on the posted rate alone.

That’s exactly where my work earns its keep. At Hypotheques.ca, I negotiate every day with more than twenty financial institutions and private lenders. And beyond the rate, we look at what really matters over five years: prepayment penalties, loan portability, payment flexibility. Over the life of a term, those conditions often weigh more than the rate itself.

Above all, I work for you, not for the bank. My role is to advise you with complete independence, numbers in hand, and to steer you toward the lender whose product genuinely serves your interests.

Renewal coming up, purchase taking shape, or simply want to validate your strategy? Book an appointment today or call us at 514-447-3000. A few calls and a few clicks can literally be worth thousands of dollars.

The rates, premiums and rules cited in this article are current as of July 2026 and may change. This content is for information purposes only and does not constitute personalized financial, tax or legal advice. Every situation deserves an individual analysis.